Press Releases

Release of 1st Quarter 2022 real estate statistics

22 April 2022

This article has been migrated from an earlier version of the site and may display formatting inconsistencies.

The Urban Redevelopment Authority (URA) released today the real estate statistics for 1st Quarter 2022.1

PRIVATE RESIDENTIAL PROPERTIES

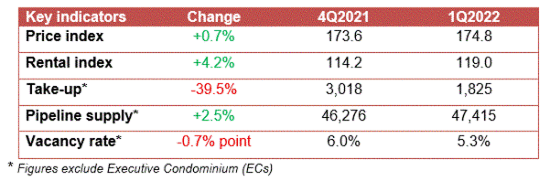

Private residential market at a glance:

Prices and Rentals

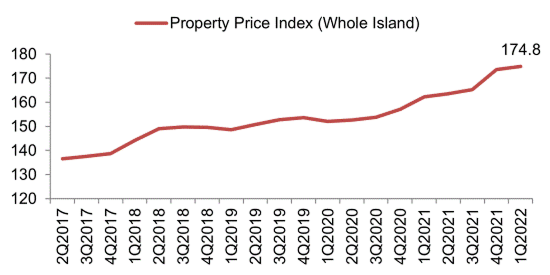

Prices of private residential properties increased by a slower pace of 0.7% in 1st Quarter 2022, compared with the 5.0% increase in the previous quarter.

Property Price Index of private residential properties

Prices of landed properties increased by 4.2% in 1st Quarter 2022, compared with the 3.9% increase in the previous quarter. Prices of non-landed properties decreased by 0.3% in 1st Quarter 2022, compared with the 5.3% increase in the previous quarter.

Prices of non-landed properties in Core Central Region (CCR) decreased by 0.1% in 1st Quarter 2022, compared with the 2.7% increase in the previous quarter. Prices of non-landed properties in Rest of Central Region (RCR) decreased by 2.7%, compared with the 6.7% increase in the previous quarter. Prices of non-landed properties in Outside Central Region (OCR) increased by 2.2%, compared with the 5.7% increase in the previous quarter (see Annexes A-1 [PDF, 8 KB], A-2 [PDF, 9 KB] & A-6 [PDF, 15 KB]2).

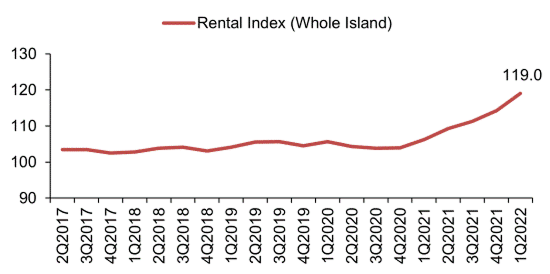

Rentals of private residential properties increased by 4.2% in 1st Quarter 2022, compared with the 2.6% increase in the previous quarter.

Rental Index of private residential properties

Rentals of landed properties increased by 5.3% in 1st Quarter 2022, compared with the 1.2% increase in the previous quarter. Rentals of non-landed properties increased by 4.1%, compared with the 2.7% increase in the previous quarter.

Rentals of non-landed properties in CCR increased by 3.8% in 1st Quarter 2022, compared with the 2.9% increase in the previous quarter. Rentals in RCR increased by 4.7%, compared with the 2.8% increase in the previous quarter. Rentals in OCR increased by 4.0%, compared with the 2.4% increase in the previous quarter (see Annexes A-3 [PDF, 8 KB] & A-4 [PDF, 10 KB]).

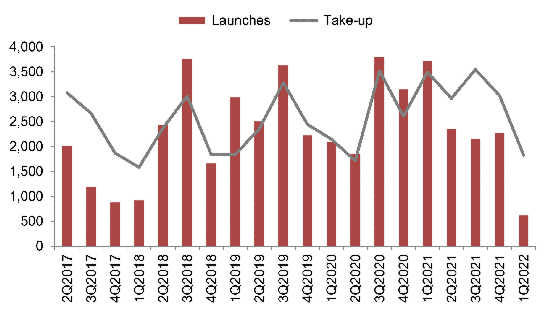

Launches and Take-up

Developers launched 613 uncompleted private residential units (excluding ECs) for sale in 1st Quarter 2022, compared with the 2,275 units in the previous quarter (see Annex C-1 [PDF, 10 KB]).

Developers sold 1,825 private residential units (excluding ECs) in 1st Quarter 2022, compared with the 3,018 units sold in the previous quarter (see Annex D [PDF, 78 KB]).

Number of private housing units launched and sold by developers (excluding ECs)

Developers did not launch any EC units for sale in 1st Quarter 2022 and sold 131 EC units in the quarter (see Annex F [PDF, 70 KB]). In comparison, developers did not launch any EC units for sale and sold 260 EC units in the previous quarter.

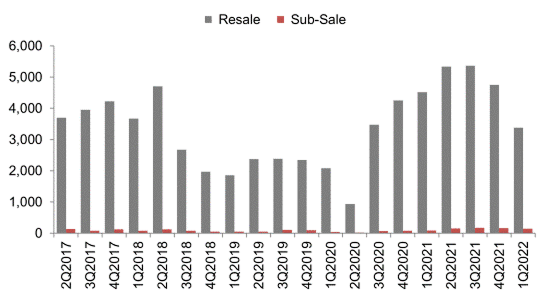

Resales and Sub-sales

There were 3,377 resale transactions in 1st Quarter 2022, compared with the 4,748 units transacted in the previous quarter. Resale transactions accounted for 63.2% of all sale transactions in 1st Quarter 2022, compared with 59.9% in the previous quarter (see Annex D [PDF, 78 KB]).

There were 141 sub-sale transactions in 1st Quarter 2022, compared with the 159 units transacted in the previous quarter. Sub-sales accounted for 2.6% of all sale transactions in 1st Quarter 2022, compared with 2.0% in the previous quarter (see Annex D [PDF, 78 KB]).

Number of resale and sub-sale transactions for private residential units (excluding ECs)

Supply in the Pipeline

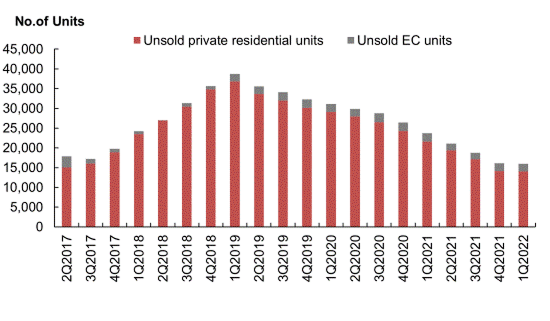

As at the end of 1st Quarter 2022, there was a total supply of 47,415 uncompleted private residential units (excluding ECs) in the pipeline with planning approvals3, compared with the 46,276 units in the previous quarter (see Annexes E-1 [PDF, 58 KB] & E-2 [PDF, 66 KB]4). Of this number, 14,087 units remained unsold as at the end of 1st Quarter 2022, compared with the 14,154 units in the previous quarter (see Annexes B-1 [PDF, 7 KB] & B-2 [PDF, 10 KB]).

After adding the supply of 5,333 EC units in the pipeline, there were 52,748 units in the pipeline with planning approvals (see Annex E-3 [PDF, 8 KB]). Of the EC units in the pipeline, 1,878 units remained unsold. In total, 15,965 units with planning approvals (including ECs) remained unsold, compared to 16,139 units in the previous quarter.

Total number of unsold private residential units in the pipeline

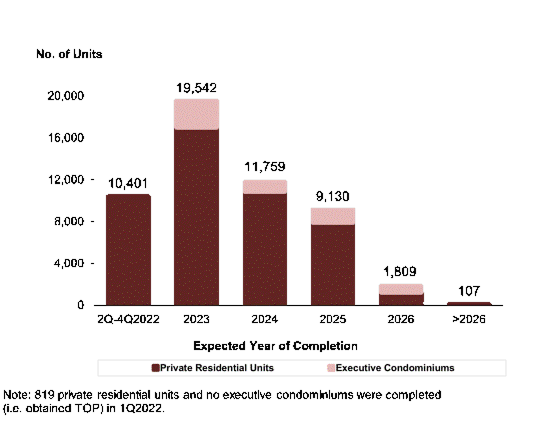

Based on the expected completion dates reported by developers, 10,401 units (including ECs) will be completed in the remaining 3 quarters of 2022. Another 19,542 units (including ECs) are expected to be completed in 2023.

Pipeline supply of private residential units and ECs (with planning approvals) by expected year of completion

Apart from the 15,965 unsold units (including ECs) with planning approval as at the end of 1st Quarter 2022, there is a potential supply of around 6,700 units (including ECs) from Government Land Sales (GLS) sites that have not been granted planning approval yet.5

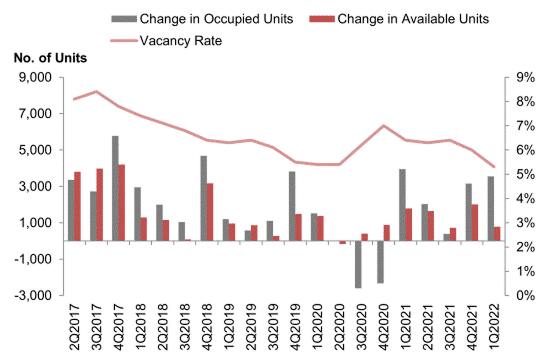

Stock and Vacancy

The stock of completed private residential units (excluding ECs) increased by 783 units in 1st Quarter 2022, compared with the increase of 2,008 units in the previous quarter. The stock of occupied private residential units (excluding ECs) increased by 3,544 units in 1st Quarter 2022, compared with the increase of 3,147 units in the previous quarter. As a result, the vacancy rate of completed private residential units (excluding ECs) decreased to 5.3% as at the end of 1st Quarter 2022, from 6.0% in the previous quarter (see Annex E-1 [PDF, 58 KB]).

Stock and vacancy of private residential units (excluding ECs)

Vacancy rates of completed private residential properties as at the end of 1st Quarter 2022 in CCR, RCR and OCR were 8.1%, 6.1%, and 3.6% respectively, compared with the 9.3%, 7.0% and 4.1% in the previous quarter (see Annex E-4 [PDF, 9 KB]).

OFFICE SPACE

Office market at a glance:

Prices and Rentals

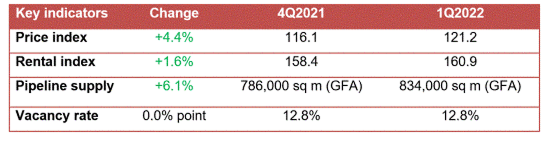

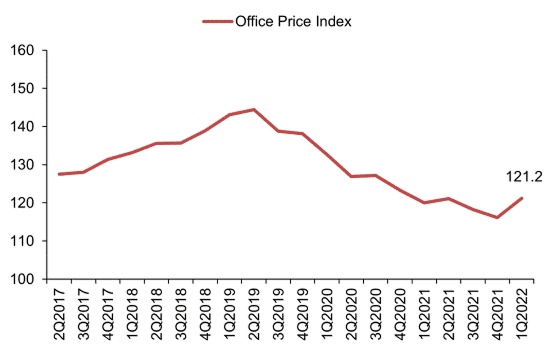

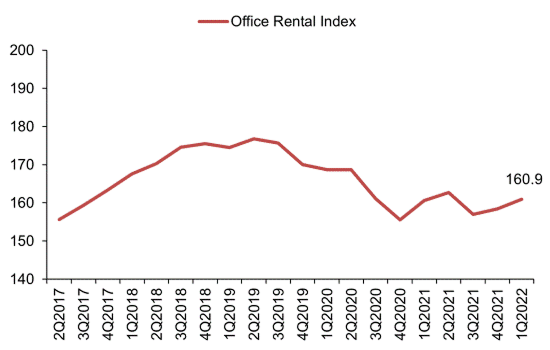

Prices of office space increased by 4.4% in 1st Quarter 2022, compared with the 1.8% decrease in the previous quarter (see Annex A-1 [PDF, 8 KB]). Rentals of office space increased by 1.6% in 1st Quarter 2022, compared with the 0.9% increase in the previous quarter (see Annexes A-3 [PDF, 8 KB] & A-5 [PDF, 73 KB]).

Property Price Index of office space in Central Region

Rental Index of office space in Central Region

Supply in the Pipeline

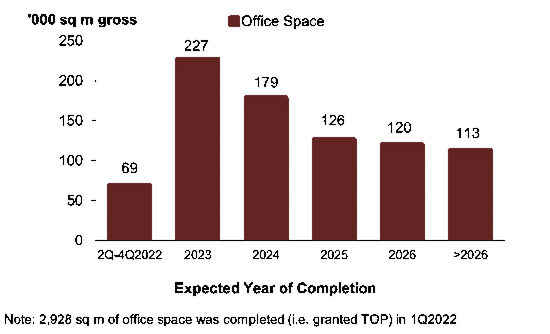

As at the end of 1st Quarter 2022, there was a total supply of about 834,000 sq m GFA of office space in the pipeline, compared with the 786,000 sq m GFA of office space in the pipeline in the previous quarter (see Annexes E-1 [PDF, 58 KB] & E-2 [PDF, 66 KB]).

Pipeline supply of office space

Stock and Vacancy

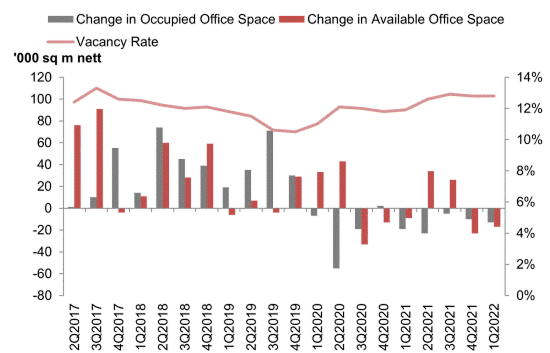

The amount of occupied office space decreased by 13,000 sq m (nett) in 1st Quarter 2022, compared with the decrease of 10,000 sq m (nett) in the previous quarter. The stock of office space decreased by 17,000 sq m (nett) in 1st Quarter 2022, compared with the decrease of 23,000 sq m (nett) in the previous quarter. As a result, the island-wide vacancy rate of office space remained unchanged at 12.8% as at the end of 1st Quarter 2022 (see Annexes A-5 [PDF, 73 KB] & E-1 [PDF, 58 KB]).

Stock and vacancy of office space

RETAIL SPACE

Retail market at a glance:

Prices and Rentals

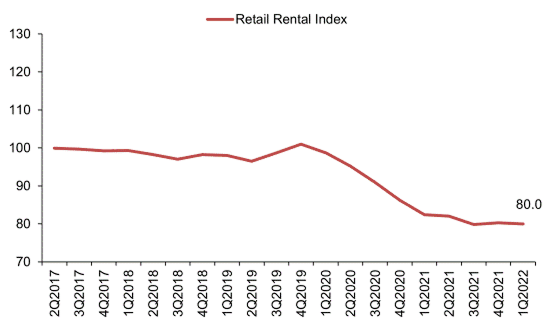

Prices of retail space decreased by 1.4% in 1st Quarter 2022, compared with the 1.9% increase in the previous quarter (see Annex A-1 [PDF, 8 KB]). Rentals of retail space decreased by 0.4% in 1st Quarter 2022, compared with the 0.6% increase in the previous quarter (see Annexes A-3 [PDF, 8 KB] & A-5 [PDF, 73 KB]).

Property Price Index of retail space in Central Region

Rental Index of retail space in Central Region

Supply in the Pipeline

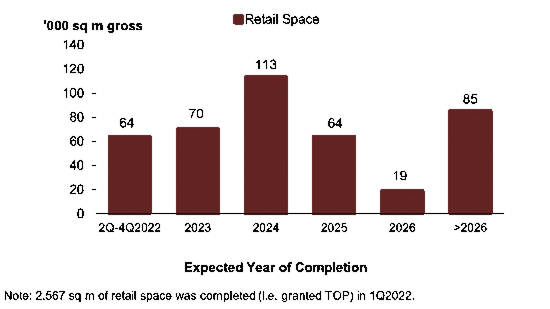

As at the end of 1st Quarter 2022, there was a total supply of 415,000 sq m GFA of retail space from projects in the pipeline, compared with the 405,000 sq m GFA of retail space in the pipeline in the previous quarter (see Annexes E-1 [PDF, 58 KB] & E-2 [PDF, 66 KB]).

Pipeline supply of retail space

Stock and Vacancy

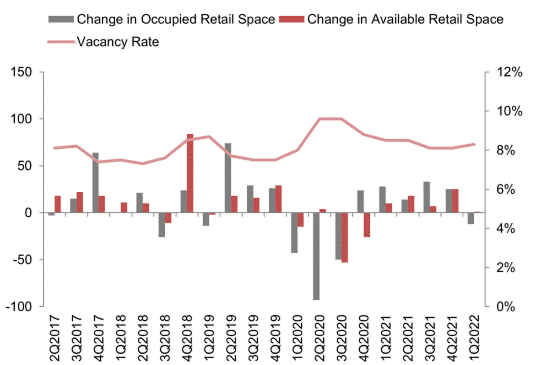

The amount of occupied retail space decreased by 12,000 sq m (nett) in 1st Quarter 2022, compared with the increase of 25,000 sq m (nett) in the previous quarter. The stock of retail space increased by 1,000 sq m (nett) in 1st Quarter 2022, compared with the increase of 25,000 sq m (nett) in the previous quarter. As a result, the island-wide vacancy rate of retail space increased to 8.3% as at the end of 1st Quarter 2022 , from 8.1% as at the end of the previous quarter (see Annexes A-5 [PDF, 73 KB] & E-1 [PDF, 58 KB]).

Stock and vacancy of retail space

URA’S REAL ESTATE INFORMATION SERVICE

More detailed information on the price and rental indices, supply in the pipeline, stock and vacancy rates of the various property sectors can be found in the Real Estate Information System (REALIS), an online database of URA.

More information on REALIS can be found at https://eservice.ura.gov.sg/reis/index.

Table caption

1 | Statistics in this press release are based on quarter to quarter comparisons, unless otherwise stated. |

|---|---|

2 | The prices of private residential properties are not uniform and vary from project to project. Home-buyers can view more detailed information on transactions of private residential properties at: https://eservice.ura.gov.sg/property-market-information/pmiResidentialTransactionSearch . Similar information can also be accessed by users on the go via URA’s iphone/ipad application. The application can be downloaded directly from https://itunes.apple.com/app/property-market-information/id573494340?mt=8 . |

3 | Projects in the pipeline are new development or redevelopment projects with planning approvals, i.e. Provisional Permission (PP) or Written Permission (WP). |

4 | More detailed data on supply in the pipeline by market segment, development status and expected year of completion can be found at https://eservice.ura.gov.sg/property-market-information/pmiResidentialPipelinePrivateUnits |

5 | These are from awarded GLS sites and Confirmed List sites that have not been awarded yet. |

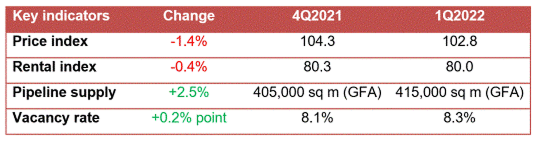

SUMMARY OF KEY INFORMATION FOR 1ST QUARTER 2022

Table caption

Annex | Title |

|---|---|

| Comparison of Property Price Index for 4th Quarter 2021 and 1st Quarter 2022 |

| Price Indices of Non-Landed Properties by Market Segment |

| Comparison of Rental Index for 4th Quarter 2021 and 1st Quarter 2022 |

| Rental Indices of Non-Landed Properties by Market Segment |

| Median Rentals and Vacancy of Office and Retail Space |

| Chart of Property Price Index by Type of Property |

| Chart of Residential Property Price Index by Type |

| Number of Unsold Private Residential Units from Projects with Planning Approvals |

| Number of Unsold Private Residential Units from Projects with Planning Approvals by Market Segment |

| Number of Uncompleted Private Residential Units Launched in the Quarter by Market Segment |

| Number of Private Residential Units Sold in the Quarter by Market Segment |

| Number of New Sale, Sub-Sale and Resale Transactions for Private Residential Units by Market Segment |

| Stock & Vacancy and Supply in the Pipeline as at End of 1st Quarter 2022 |

| Supply in the Pipeline by Development Status and Expected Year of Completion as at End of 1st Quarter 2022 |

| Pipeline Supply of Private Residential Units and Executive Condominiums by Expected Year of Completion as at End of 1st Quarter 2022 |

| Vacancy of Private Residential Units by Market Segment |

| Number of Executive Condominium Units Launched and Sold in the Quarter |